Market Forecast for 2024 according to Royal LePage

Royal LePage predicts minor interest rate cuts to fuel national aggregate home price increase of 5.5% year over year in fourth quarter of 2024*

Highlights:

- Nationally, single-family detached and condominium prices forecasted to increase 6.0% and 5.0%, respectively, year over year in Q4 of 2024

- Home prices are expected to show greatest increases in second half of 2024

- Calgary aggregate home price projected to see greatest gains of all major markets at 8.0%

- Aggregate price of a home in the greater regions of Toronto and Montreal are forecast to end next year 6.0% and 5.0% respectively above the final quarter of 2023, while Greater Vancouver is expected to see a more modest increase of 3.0%

- Royal LePage forecast based on expectation that Bank of Canada will hold rates steady through first half of next year, and begin modestly easing rates in late summer or fall

Home prices are expected to rise next year in all major markets across the country, with Calgary forecast to see the greatest gains. Throughout the second half of 2023, while prices have been declining in other cities, the Calgary real estate market has bucked the trend continuing on an upward price trajectory.

Royal LePage’s forecast is based on the prediction that the Bank of Canada has concluded its interest rate hike campaign and that the key lending rate will hold steady at five per cent through the first half of 2024. The central bank is expected to start making modest cuts in late summer or fall of next year. Meanwhile, several major financial institutions have already begun offering discounts on fixed-rate mortgages.

“For the last year, many Canadians have been fixated on the idea of interest rates needing to come down significantly before they can afford to enter or re-enter the housing market. Acceptance that a mortgage rate of four to five per cent is the new normal should untether pent-up demand as first-time buyers, flush with savings collected during the extended down market in housing, regain the confidence to go home shopping. And, with the return of first-timer demand, we expect families who have put off upgrading their homes to begin to list their properties in much greater numbers,” continued Soper.

How we got here

Over the last eighteen months, sales activity in most of Canada’s major real estate markets has been on the decline, while inventory levels have gradually increased. While transactions are down as much as 20 or 30 per cent in some regions, home prices have only declined modestly during this time, due to a simultaneous drop in demand as buyer hopefuls continue to hold out for lower interest rates. Still, prices remain above 2022 levels.

“Canada’s real estate market has been on a roller coaster ride for the last four years. A global pandemic briefly brought market activity to a grinding halt in early 2020, followed by a rapid, widespread spike in demand and price appreciation as Canadians sought safety and greater living space in their homes among a world of uncertainty. By the spring of 2022, home prices had reached unprecedented highs, but when interest rates started rising quickly and steeply to combat inflation, the extended market correction began,” said Soper. “Markets take time to adjust. We see a move toward typical home sale transaction levels in 2024, and as the year progresses, appreciating house prices.”

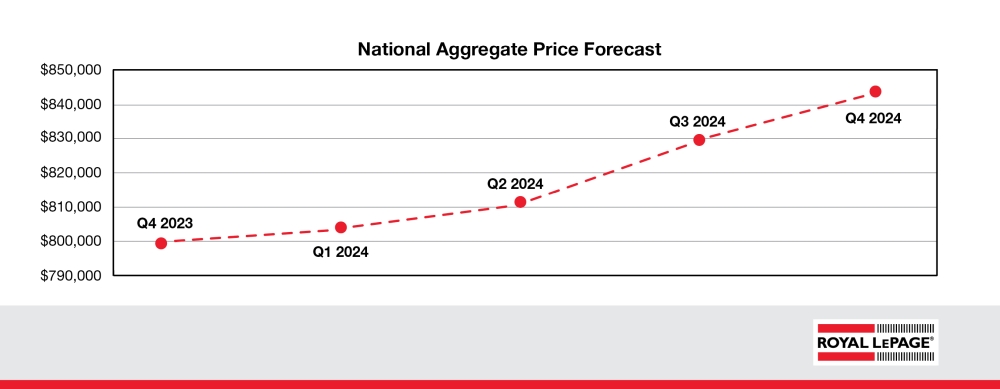

Quarterly forecast

Nationally, home prices are forecast to see modest quarterly gains in the first two quarters of 2024, with more considerable increases expected in the second half of the year, following the anticipated start of interest rate cuts by the Bank of Canada. The aggregate price of a home in Canada is forecast to be 3.3 per cent higher in Q1 of 2024 compared to the same quarter in 2023, reflecting a 0.5 per cent increase over the fourth quarter of 2023. In the second quarter of next year, the national aggregate home price is forecast to be 0.2 per cent higher year over year and 0.9 per cent above the previous quarter. In the third quarter, home prices are expected to be 3.3 per cent higher year over year and 2.3 per cent higher on a quarterly basis. And, in the fourth quarter of 2024, the national aggregate price of a home is expected to land 5.5 per cent above the same quarter in 2023, an increase of 1.7 per cent quarter over quarter. Based on this forecast, by the end of next year, home prices will have essentially climbed back to their pandemic peak, reached in the first quarter of 2022.

Supply shortage and affordability challenges

Canada continues to struggle with a chronic housing supply shortage. According to the Canada Mortgage and Housing Corporation, the country needs about 3.5 million additional housing units by 2030 to restore affordability, with the greatest need concentrated in the provinces of Ontario and British Columbia.[3] At the current pace of housing construction and considering the rate of new household formation and immigration projections, inventory will remain out of step with projected demand for years to come.

“For many years, condominiums have offered an affordable opportunity for entry onto the real estate ladder, in addition to their ‘lock and leave’ lifestyle that is typically attractive to young people. Of late, however, this segment of the market has also become out of financial reach for many in major cities like Toronto and Vancouver, where new construction cannot keep pace with growing demand. And, the elevated cost of construction materials and labour are adding additional pressure on builders,” said Soper. “What’s more, with ultra-low vacancy rates, the rental market is not the escape route many would-be buyers hope it could be, with monthly lease rates on the rise from coast to coast.”

Competing public policy objectives

In the federal government’s Fall Economic Statement released last month, billions of dollars were committed and reaffirmed towards increased levels of new housing construction. This includes favourable loan agreements and tax benefits for developers of purpose-built rental buildings and public housing projects, as well as financial assistance for municipalities to crack down on short-term rentals in an effort to push more supply onto the resale market in urban centres.[4]

“It is encouraging to see policy makers tackling Canada’s housing affordability issues and supply shortfall, yet there remains a large accessibility gap for first-time buyers and middle-income earners. Those that have salaries or wages that have not kept up with the cost of living find it difficult to achieve the dream of home ownership. Thankfully, many have received financial help from family or friends, yet this is not something Canadians should have to rely upon,” said Soper. “With competing policy objectives – record-high immigration to combat labour shortages, for example – I see little hope that housing construction will meet that need this decade. The demand/supply imbalance will put further upward pressure on home prices.

“While uncomfortably expensive housing in our major markets is inevitable, it is imperative that governments adopt quick and extraordinary measures to mitigate affordability challenges and address the housing supply crisis,” concluded Soper.

MARKET SUMMARIES

Calgary

In Calgary, the aggregate price of a home in the fourth quarter of 2024 is forecast to increase 8.0 per cent year over year to $711,612, the highest of all forecast regions. During the same period, the median price of a single-family detached property is expected to rise 6.0 per cent to $803,692, while the median price of a condominium is forecast to increase 9.5 per cent to $286,562.

“Although activity has slowed in Calgary, home prices have not dipped like they have in other cities across Canada, due to a sustained shortage of supply,” said Corinne Lyall, broker and owner, Royal LePage Benchmark. “If rates start to come down in the second half of 2024 – as they are predicted to do – it will motivate buyers to jump into the market as their borrowing power improves. Many homeowners will see their mortgages come up for renewal next year, and will be forced to take a higher interest rate. This may push some more inventory onto the market, as overleveraged borrowers downsize in an effort to get some relief from higher monthly payments.”

Lyall noted that Calgary has seen a slowdown in the number of interprovincial buyers relocating to the city compared to the past few years. However, investors from other provinces continue to look for real estate opportunities in the Prairies, driving demand in the multi-family segment.

“We expect that home prices will rise over the next year, and will outperform other major cities as Calgary’s relative affordability continues to attract buyers to the city. A shortage of supply remains a challenge, which will keep prices on an upward trajectory for the foreseeable future as buyers compete for the few homes available,” said Lyall. “Heading into the new year, I predict that we will see a slow start to the market in January and February, a similar pattern to what we saw in early 2023. Once March arrives, buyers and sellers will move off of the sidelines as a brisk spring market begins and consumer confidence strengthens.”

Edmonton

In Edmonton, the aggregate price of a home in the fourth quarter of 2024 is forecast to increase 4.0 per cent year over year to $443,248. During the same period, the median price of a single-family detached property is expected to rise 7.0 per cent to $493,805, while the median price of a condominium is forecast to increase 2.0 per cent to $192,678.

“Next year, we expect similar activity to this year, but home values will likely increase as price appreciation falls in line with historical trends. Edmonton continues to experience a shortage of homes relative to demand, which will keep home prices trending upward in 2024. This will only be intensified by the number of residents moving into the city, searching for affordability and work opportunities,” said Tom Shearer, broker and owner, Royal LePage Noralta Real Estate. “We continue to see a gap between buyer expectations and the reality of how far their dollar will stretch. Until they feel that they’re getting their money’s worth, some buyers will continue to wait on the sidelines, building further pent-up demand.”

Shearer noted that Edmonton home prices are largely tied to the oil and gas sector, which continues to be a major driver of employment opportunities. Edmonton has seen a surge in newcomers over the past few years, in addition to Canadians moving to Alberta from other provinces – namely Ontario and British Columbia.

“The city’s fast-growing population has put upward pressure on home prices,” said Shearer. “In recent years, the province has seen a notable surge in activity and home prices in the city of Calgary, and we believe similar trends are on the horizon for Edmonton.”

Greater Toronto Area

In the Greater Toronto Area, the aggregate price of a home in the fourth quarter of 2024 is forecast to increase 6.0 per cent year over year to $1,198,012. During the same period, the median price of a single-family detached property is expected to rise 7.0 per cent to $1,481,950, while the median price of a condominium is forecast to increase 5.0 per cent to $754,845.

“There is a lot of uncertainty surrounding Canada’s economy and the real estate market these days, and that is especially true in the major centres like Toronto. What is certain is that Canadians need housing, they value home ownership and most are willing to prioritize buying a home over just about anything else,” said Karen Yolevski, chief operating officer, Royal LePage Real Estate Services Ltd. “We know there are still buyers on the sidelines waiting for interest rates to come down. What is unclear is how many can afford to jump back into the market at the first sign of a reduction, and how many truly cannot afford to transact in this environment.”

Yolevski added that a lot of future activity will be dependent not only on reduced interest rates, but the timing of mortgage renewals. Many would-be move-up buyers who have enjoyed ultra-low rates for the past few years will be willing to make a move as their current loan terms expire. No longer bound to their current property because of the interest rate, more of these owners will put their properties on the market and begin their search for a new home.

“The GTA is Canada’s most densely-populated region and continues to be the top destination for newcomers. Despite a temporary drop in sales, there remains a huge gap in the number of homes available and those needed to satisfy demand from middle-income earners. This continues to put significant pressure on the already-tight rental market.”

Yolevski also noted that investor-owned properties, namely condominiums, could add supply to the market over the next year or two, as mortgages come up for renewal and owners choose to sell rather than renew at a higher rate.

“If tenanted properties are not producing positive cash-flow, investors may choose to sell rather than renew their mortgages in this higher-cost borrowing environment. This, in addition to new legislation that incentivizes the development of purpose-built rental properties, could add some much-needed inventory to the entry-level market,” said Yolevski. “It will not be enough, however, to put downward pressure on prices.”

Greater Montreal Area

In the Greater Montreal Area, the aggregate price of a home in the fourth quarter of 2024 is forecast to increase 5.0 per cent year over year to $610,260. During the same period, the median price of a single-family detached property is expected to rise 4.5 per cent to $684,998, while the median price of a condominium is forecast to increase 6.0 per cent to $471,912.

“The real estate crystal ball prediction will be made up of many factors in 2024, but the thing to remember is that the reduction in inflation closer to the target rate will not have been enough to curb the increase in real estate prices for very long, due to a chronic lack of supply,” said Dominic St-Pierre, vice-president and general manager, Royal LePage, Quebec region. “Housing is an essential need, and the still-critical shortage of units required to meet demand and population growth is destined to persist, as long as investments by all levels of government fail to materialize in the urban landscape. However, even if interest rates are expected to start dipping next year, consumers will have to adapt to a new reality, as the days of ultra-low rates are over. In the short term, this should keep property price increases in check while households adjust their purchasing behaviours.”

In its fall economic update, the Quebec government pledged $1.8 billion over five years to improve access to housing in the province.[5] This investment will include actions to accelerate the construction of affordable housing, as well as assistance to municipalities in the form of increased flexibility in urban planning bylaws, measures to facilitate the construction of secondary suites, and support for the training of the construction workforce.

“We welcome any initiative aimed at reducing the gap between supply and demand, and applaud the creativity of the various levels of government in multiplying solutions,” said St-Pierre. “However, the challenge is massive, since Quebec requires the addition of more than 1.2 million units by the end of the decade in order to regain some semblance of affordability.”

What’s more, Montreal is the Canadian city where housing starts fell the most in the first six months of 2023, a 26-year record, and the prognosis for 2024 is not optimal.[6] Rising borrowing costs have taken a heavy toll on builders’ and developers’ portfolios over the past year. For this reason, it is expected that when interest rates start to decline, the pent-up demand will unleash on the condominium segment in the Greater Montreal Area, which will see an appreciation rate slightly higher than that of single-family homes.

“In addition to condominiums, the market for single-family homes priced at $1 million and higher should also see an upturn as expectations of lower interest rates materialize,” said Marc Lefrançois, chartered real estate broker, Royal LePage Tendance in Montreal. “For this category of buyers, moving from one property to another is often not an immediate necessity. Many have therefore preferred to wait in order to take advantage of more favourable financing conditions, but could return to the market quickly when the central bank announces the start of a downward cycle in interest rates.”

Economic conditions in the province were heavily weighed down at the end of the year by the outbreak of strikes in the public sector, as well as numerous layoffs across a myriad of industries, which could influence consumer confidence regarding large purchases such as a property in 2024, despite a widely expected drop in interest rates.

“Savings accumulated by households during the pandemic have begun to run out, keeping pace with inflation and interest rate hikes over the past 21 months,” noted St-Pierre. “Quebec households have a high level of debt, and despite signs of relief in borrowing costs on the horizon, their purchasing power will remain limited. The downward adjustment of the Bank of Canada’s overnight rate, even by a quarter per cent, could send a strong message to consumers about future economic conditions. The pace at which interest rates rebalance will also play a big part in the equation,” he continued.

St-Pierre added, “The start of 2024 could see the Greater Montreal Area’s real estate market get off to a slow start, following a similar trend to the last quarter of 2023. But, we expect the recovery to get underway quickly once interest rates start to fall. Next year is likely to be more active than 2023 in terms of property sales,” he concluded.

Greater Vancouver

In Greater Vancouver, the aggregate price of a home in the fourth quarter of 2024 is forecast to increase 3.0 per cent year over year to $1,281,732. During the same period, the median price of a single-family detached property is expected to rise 2.5 per cent to $1,778,785, while the median price of a condominium is forecast to increase 4.0 per cent to $795,808.

“Activity has slowed in recent months allowing some inventory to build, as buyers hold out for a deal or for interest rates to drop, and sellers continue to expect 2021 values for their homes. While this has resulted in a market slowdown, Greater Vancouver could see a brisk spring if interest rates remain steady or dip even a little,” said Randy Ryalls, managing broker, Royal LePage Sterling Realty. “There is still plenty of demand waiting in the wings, and a glimmer of light at the end of the tunnel could easily heat up the market again. Some buyers will rush to transact before the competition gets too tight. Others will wait for multiple rate cuts.”

Ryalls noted that while many sidelined buyers are likely to jump back into the market next year if lending rates come down, competition will not be as aggressive as it was two years ago when borrowing costs sat at record lows.

“Purchasing power has been deflated. With the rising cost of living and interest rates five or six times higher than they were a few years ago, buyers have less capacity to outbid their competitors. This will keep a lid on price appreciation, even as activity picks up,” said Ryalls. “Some banks have already begun to offer discounts on fixed-rate mortgages, incentivizing some buyers back to the table. Eventually, everyone will have to adjust to the new realities of the market.”

Ottawa

In Ottawa, the aggregate price of a home in the fourth quarter of 2024 is forecast to increase 4.5 per cent year over year to $771,942. During the same period, the median price of a single-family detached property is expected to rise 4.0 per cent to $884,000, while the median price of condominium is forecast to increase 5.0 per cent to $407,190.

“The Ottawa market is heavily influenced by interest rates. Even if we see only a modest decrease in rates by the Bank of Canada mid-way through 2024, this move could spark a flurry of buying activity leading into our late summer and early fall market,” said Jason Ralph, broker of record, Royal LePage Team Realty. “These days, only those homeowners who must move for personal reasons are listing their homes. In many cases, those with the luxury of time are staying on the sidelines, waiting for interest rates to come down. This is creating pent-up buyer demand, especially in the always desirable single-family detached segment.”

Ralph noted that many first-time homebuyers have been renting as they wait for lower interest rates and improved purchasing power. This is creating a competitive rental market, especially as newcomers relocate to Ottawa for opportunities in the city’s thriving public service job market, adding to the already high levels of renter demand.

“Though we have returned to a more normalized market post-pandemic, we are not quite in balanced territory yet as demand continues to outweigh supply. As a result, we are expecting a brisk spring market next year,” said Ralph. “Should we see a drop in interest rates, market activity will intensify, resulting in an incline in home prices in the later months of the year and into 2025.”

Halifax

In Halifax, the aggregate price of a home in the fourth quarter of 2024 is forecast to increase 3.0 per cent year over year to $521,592. During the same period, the median price of a single-family detached property is expected to rise 5.0 per cent to $602,490, while the median price of a condominium is forecast to increase 1.5 per cent to $431,375.

“Looking ahead to the 2024 housing market in Halifax, we are feeling quite positive. It is likely that interest rates will be reduced mid-year, which will cause some hesitant or sidelined buyers to jump back into the market,” said Matt Honsberger, broker and owner, Royal LePage Atlantic. “Those in the rental market – who are currently paying higher-than-normal prices due to tight competition in this segment – will be especially motivated to transition into home ownership. Many move-up buyers, who have patiently been biding their time until borrowing rates improve or their mortgages come up for renewal, are also expected to re-enter the market in the new year.”

Honsberger noted that investors from Ontario and Alberta are an active buyer group in Nova Scotia. This demand is not exclusive to the investor-friendly condominium segment, but is also present in the single-family and new construction markets as well, despite the non-resident tax applicable to all transactions by out-of-province buyers.

“Though we will experience the typical seasonal slowdown in the first weeks of the new year, I expect January will still be up in terms of prices and activity compared to the same time this year. Sales are likely to begin increasing in February and March, as more inventory comes online. And, if we see one or two rate cuts in the fall, a boost of activity will follow,” said Honsberger.

Winnipeg

In Winnipeg, the aggregate price of a home in the fourth quarter of 2024 is forecast to increase 3.0 per cent year over year to $396,447. During the same period, the median price of a single-family detached property is expected to rise 4.0 per cent to $440,232, while the median price of a condominium is forecast to increase 2.0 per cent to $263,568.

“Every year, the Winnipeg real estate market follows a similar pattern – slow through the winter months with a rise in activity in the spring, followed by a quieter summer and then a slow decline for the remainder of the year. We expect 2024 will look much like a typical year, resulting in modest price increases as consumer confidence strengthens,” said Michael Froese, broker and manager, Royal LePage Prime Real Estate. “Single-family detached homes will likely see the majority of next year’s price growth, especially in the highly-sought-after $300,000 to $400,000 price range.”

Froese added that he is not overly concerned that the expected wave of upcoming mortgage renewals will force many homeowners to have to list their homes due to higher monthly costs.

“As has always been the case, Canadians value home ownership. When faced with financial strain, most people will cut back on discretionary spending and make other concessions before resorting to selling their homes,” he added. “While it may not be as strong of a seller’s market as it was two years ago, prices are anticipated to remain buoyant as buyer demand is expected to continue outweighing available home supply, even in the slower months.”

Regina

In Regina, the aggregate price of a home in the fourth quarter of 2024 is forecast to increase 3.0 per cent year over year to $381,306. During the same period, the median price of a single-family detached property is expected to rise 4.0 per cent to $417,456, while the median price of a condominium is forecast to increase 2.5 per cent to $228,063.

“Like many cities across Canada, higher interest rates have prompted buyers to hit pause as their borrowing capacity has diminished. As a result, demand is building on the sidelines as consumers wait anxiously for borrowing costs to come down,” said Shaheen Zareh, sales representative, Royal LePage Regina Realty. “Although it is highly unlikely we will see rates as low as one or two per cent again – at least not anytime soon – I do believe some of that sidelined demand will re-enter the market once rates are cut, even if only by a small amount.”

Zareh added that rental prices have climbed in Regina as higher mortgage rates have kept would-be buyers in leased properties for longer. This has constrained rental supply and pushed prices up, making the cost of monthly rent comparable to a mortgage payment in some cases.

“Overall, supply remains constrained. I expect prices will see a modest increase in 2024, not only in the detached segment but in the condo market as well. There has been a lot of activity in the condominium segment as of late, despite the property type not being particularly popular in the region, historically. We have seen an uptick in condo sales thanks to first-time buyers who are seeking a more affordable option that will allow them to get a foot on the property ladder sooner.” said Zareh. “Many young buyers would much prefer a new condo for $200,000 over a detached fixer-upper that costs $100,000 more.”

Zareh noted that many short-term pandemic-era mortgages are expected to come up for renewal next year, which could have an impact on supply as homeowners weigh the decision to renew or sell their homes and downsize into a more financially manageable property.

*This particular article was reposted from a press release by Royal LePage Canada in December 2023.

Keith Pushor has been a licensed Realtor since 1994 servicing the Lethbridge and area market. He publishes a semi-regular BLOG about news and adventures in his real estate practice, cycling, and our outdoor environments in general. The information presented in this BLOG, while being reliable, is ultimately only the perspectives and opinions of Keith Pushor, may or may not have been assisted by ChatGPT Technology, and do not necessarily reflect those of LDAR or Royal LePage South Country.